Overview

Introduction

Tether (USDT) is a dollar-pegged stablecoin issued by Tether International for moving tokenized dollars across crypto networks.

Tether is best understood as a crypto-market dollar substitute, not as a bank deposit. Its main token, USD₮ or USDT, is designed to trade near $1 while moving on public blockchains such as Ethereum, Tron, Solana, Avalanche, and TON. Tether is reserve-backed and publishes reserve information, but holders still face issuer, redemption, regulatory, and network risks.

Key Takeaways

- What it is. Tether is the issuer behind USDT, a fiat-backed stablecoin designed to track the U.S. dollar.

- Why it matters. USDT is one of crypto’s main liquidity rails for trading, payments, treasury transfers, and dollar access outside banking hours.

- Main risk or limitation. USDT depends on Tether’s reserves, redemption rules, legal powers, and supported blockchains, rather than deposit insurance.

What Is Tether and Why Does USDT Matter?

Tether is both a company and a product family. USDT is its largest token, a blockchain asset pegged 1-to-1 with the U.S. dollar and backed by Tether's reserves. In everyday usage, most people say “Tether” when they mean USDT specifically.

USDT matters because it gives crypto users a tokenized dollar unit that works inside exchanges, wallets, DeFi protocols, and cross-border payment flows without touching the traditional banking system. A trader can sell Bitcoin into USDT without moving back to a bank account. A user can send USDT across a supported network faster than a bank wire. A market maker can quote prices in a unit that behaves more like dollars than volatile crypto assets.

One legal distinction matters before anything else. USDT is not fiat currency, is not legal tender, and is not covered by Federal Deposit Insurance Corporation protection or similar schemes in other jurisdictions. Direct issuance and redemption through Tether require a verified Tether customer account. For live USDT price, supply, and volume data, CryptoSlate's Tether market page is the current reference.

How USDT Keeps Its Dollar Peg

USDT's peg is maintained through a combination of reserves, redemption access, exchange liquidity, and market arbitrage. Understanding each layer is what separates USDT holders who know their actual exposure from those who assume it works like a savings account.

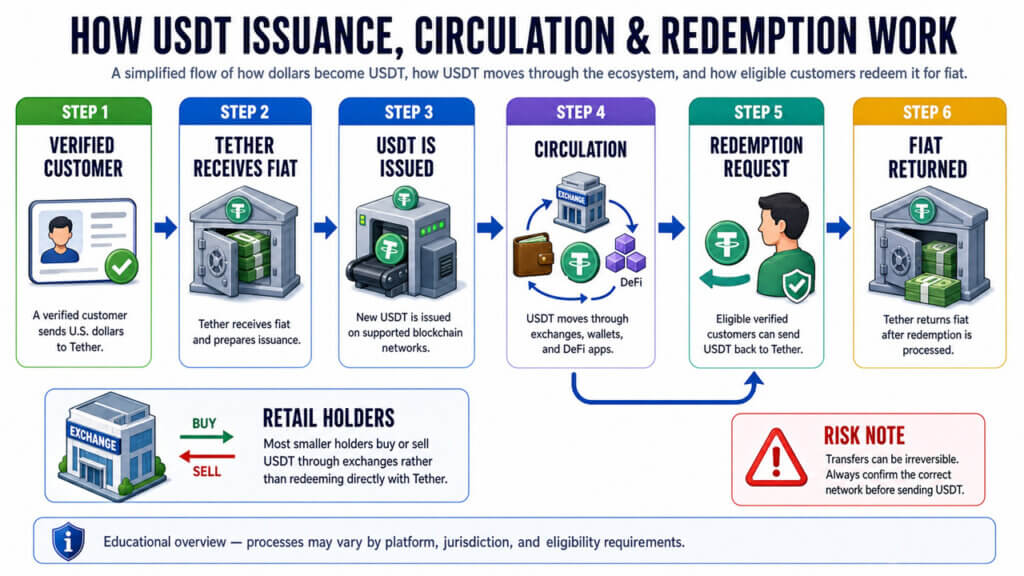

Tether issues new USDT when approved customers buy it. Those tokens then circulate through exchanges, OTC desks, wallets, and blockchain apps. Eligible verified customers can also redeem USDT for fiat through Tether's site, subject to minimums and fees. Most retail users never interact with Tether directly; they buy, sell, and exit through exchanges or brokers.

That creates two distinct pricing layers. The first is Tether's contractual redemption route for verified customers. The second is secondary-market pricing on exchanges. If USDT trades below $1, professional traders may buy discounted tokens and redeem or sell them where the price is closer to $1. If it trades above $1, new issuance and market selling can pull the price back down. The peg depends on that arbitrage functioning in normal market conditions.

The redemption route is not designed for small casual transactions. The minimum acquisition or redemption amount is $100,000, with a redemption fee equal to the greater of $1,000 or 0.1%, a 0.1% acquisition fee, and a $150 verification fee in USDT. For smaller holders, exchange liquidity is usually the practical on-ramp and off-ramp.

Where Tether Runs: Ethereum, Tron, Solana, and Other Networks

USDT is not tied to one blockchain. As of Dec. 31, 2025, Tether tokens were available on 13 blockchains: Ethereum, Tron, TON, Liquid, Solana, Avalanche, Tezos, Near, Cosmos, Celo, Kaia, Aptos, and Polkadot Asset Hub.

The network choice is not a detail you can ignore. USDT on Ethereum is an ERC-20 token. USDT on Tron uses Tron rails. USDT on Solana uses Solana infrastructure. Exchanges and wallets must support the exact network you choose. Sending USDT to the wrong network or an incompatible address can result in permanently lost funds.

Tether can also drop support for networks entirely. On Sep. 1, 2025, it stopped redeeming USDT on Omni, Bitcoin Cash SLP, Kusama, EOS, and Algorand. EUR₮ redemptions stopped on Nov. 27, 2025. Tokens on those networks may still appear in a wallet, but official redemption, exchange support, and migration options vary by network and are not guaranteed.

Network choice also affects cost. Cheaper routes are not always safer if your receiving wallet, exchange, or compliance environment does not support that network.

What Is USDT Used For?

USDT has several distinct use cases that reflect how different parts of the crypto market depend on it.

Trading liquidity is the largest. USDT pairs let traders move between Bitcoin, Ethereum, Solana, altcoins, and fiat-like balances without leaving crypto rails. The result is a dollar unit that trades around the clock across markets that do not always have local bank access.

Cross-border payments are a real secondary use. A freelancer, exchange customer, or merchant may prefer USDT because it can settle faster than a bank transfer and may be easier to receive in countries with dollar shortages or unstable local currencies. The constraint is that settlement is final once sent, and the recipient still needs a way to hold, spend, or convert the token.

DeFi applications add a third use case. USDT can be used in liquidity pools, lending protocols, perpetual futures margin, and cross-chain apps. Each of those adds smart-contract, oracle, liquidation, and bridge risk on top of the Tether-specific risks already in play.

Treasury and institutional inventory rounds out the picture. Exchanges, OTC desks, payment processors, and trading firms use USDT to settle obligations, quote prices, and rebalance liquidity across venues. Teams comparing venues for that kind of use can start with CryptoSlate's crypto exchanges hub.

How To Earn USDT

USDT does not generate staking rewards by itself. It is a reserve-backed token issued on multiple blockchains, not a proof-of-stake asset with validator mechanics built in. That means any yield on USDT comes from third-party products, not from Tether's own token design.

The routes below range from exchange earn products to DeFi protocols. Each one involves a counterparty that is not Tether, and each carries different terms, custody arrangements, and exit conditions. A product marketed as “USDT staking” is almost always one of these, regardless of how the label is worded.

| Method | How It Works | Native Or Third-Party? | Main Risk |

|---|---|---|---|

| Exchange Earn Products | A platform lets customers deposit USDT into flexible or fixed-term products and earn daily rewards. | Third-party | Custody risk, platform risk, variable terms, lockups, and regional restrictions |

| Lending Products | A platform or lending product uses deposited USDT as lending supply. Subscribed crypto is locked as lending supply and may be lent to platform borrowers when a bid succeeds. | Third-party | Counterparty risk, custody risk, redemption delays, and borrower demand changes |

| DeFi Money Markets | Users supply USDT to a smart-contract protocol and receive interest-bearing aTokens that earn interest from borrowers. | Third-party protocol | Smart contract risk, oracle risk, liquidity risk, and governance changes |

| Liquidity Pools | Users pair USDT with another asset in an automated market maker pool and may earn trading fees or incentives. Liquidity-provider risks include impermanent loss, market volatility, out-of-range positions, smart contract vulnerabilities, and fee variability. | Third-party protocol | Smart contract risk, impermanent loss, fee variability, and token-pair risk |

| Payment Or Rewards Programs | Some payment programs pay rewards in USDT. Bybit Card Rewards calculates USDT cashback from accumulated points under its rewards formula. | Third-party | Program changes, eligibility rules, custody risk, and spending limits |

| Promotional Campaigns | Exchanges sometimes run time-limited campaigns that distribute USDT vouchers or reward pools. USDT rewards can be regional, conditional, and finite. | Third-party | Expiry, qualification rules, low predictability, and chasing rewards over risk management |

Faucets are not a reliable earning route. Many “free USDT” sites are unverified, require clicks or deposits, or create phishing risk. This guide does not recommend faucet sites. Treat any faucet claim as a security check first and an earning opportunity last.

Can You Stake USDT?

No. USDT cannot be staked natively because it is a reserve-backed stablecoin issued across multiple blockchain networks, not a proof-of-stake asset that pays validator rewards to token holders.

When exchanges or apps use the term “USDT staking,” they usually mean something else entirely. The actual activity is one of the following:

- Lending USDT to a centralized platform or borrower pool

- Depositing USDT into an exchange earn product with flexible or fixed terms

- Supplying USDT to a DeFi money market protocol

- Providing USDT as one side of a liquidity pool pair

The risk profile changes depending on the product. A native staking asset pays rewards from a network's consensus mechanism, which is governed by on-chain rules. A USDT yield product pays from borrower interest, liquidity fees, exchange incentives, or promotional budgets, and any of those can stop, change rate, or become unavailable by region without notice.

Before depositing into any USDT yield product, it is worth checking: who holds custody, whether there are redemption limits or lockup periods, whether the product is available in your country, and what the smart contract or counterparty risk looks like. A higher displayed rate does not remove those constraints.

What Backs Tether? Reserves, Reports, and Open Questions

Tether's reserves back the fiat-denominated tokens it issues. Tether tokens are pegged 1-to-1 with matching fiat currencies and Tether publishes reserve information daily.

The most recent reserve report available during this review was Tether International's Financial Figures and Reserves Report as of Dec. 31, 2025. Reserves for Tether tokens in circulation amounted to $192.88 billion, while company liabilities were $186.54 billion, leaving assets exceeding liabilities by about $6.34 billion at the reporting date. Of those liabilities, $186.45 billion related to digital tokens issued.

Tether's reserve mix matters because not all backing assets behave like cash. The breakdown included $122.33 billion in U.S. Treasury bills, $19.28 billion in overnight reverse repurchase agreements, $5.55 billion in term reverse repurchase agreements, and $33.95 million in cash and bank deposits. It also included $17.45 billion in precious metals, $8.43 billion in Bitcoin, $2.76 billion in other investments, and $17.04 billion in secured loans.

Treasury bills and repo agreements are generally more liquid than gold, Bitcoin, secured loans, or other investments. Those less liquid assets add price, collateral, and liquidation risk that short-term Treasuries do not carry.

The report also has limits. The reporting date is a single point in time, Dec. 31, 2025 at 11:59 pm UTC, and BDO did not provide assurance at any other date or time. The financial figures report uses IFRS recognition and measurement principles but does not include enough information to comply fully with IFRS financial-statement presentation and disclosure requirements. The reserve report is a dated, category-level view, not a full ongoing audit of the company, its controls, or its counterparties.

Risks That Make USDT Different From Dollars in a Bank

For a stablecoin, USDT carries a layered risk profile that most beginners do not fully map out before using it. The risks are distinct and can compound each other.

Issuer risk is the foundation. USDT depends on Tether's ability and willingness to maintain reserves, process eligible redemptions, manage counterparties, and comply with applicable law. A dollar in a government-insured bank account and a USDT token on a public blockchain are different legal claims backed by different systems.

Reserve risk follows from the reserve composition. The Dec. 31, 2025 report showed Tether held significant amounts in gold, Bitcoin, secured loans, and other investments alongside its Treasury and repo holdings. Those assets may be valuable under normal conditions, but they carry price, collateral, and counterparty risk that short-term Treasuries do not.

Redemption risk affects ordinary users more than the minimum thresholds suggest. Direct redemption with Tether requires a verified account and a $100,000 minimum. That means most retail holders exit through exchange liquidity, not a direct claim on Tether. If an exchange restricts withdrawals, loses banking access, or removes a USDT pair, the path back to fiat narrows fast.

Network risk is entirely separate from what Tether holds in reserves. USDT transfers are irreversible. Sending tokens to a wrong address, an unsupported network, or a compromised wallet means accepting the risk of permanent loss. Always verify the exact network and address before transferring, and send a test amount first if the destination is unfamiliar.

Issuer-control risk is explicit in Tether's terms. Tether can freeze tokens, blacklist addresses, and deliver property to government or law enforcement authorities when circumstances warrant. In April 2026, Tether supported the U.S. government in freezing $344 million in USDT across two addresses, part of its cooperation with more than 340 law enforcement agencies in 65 countries.

Regulatory risk varies by region and is not static. A user in the EEA, the United States, Latin America, or Asia may face different exchange listings, redemption routes, tax treatment, and compliance requirements. The token can move globally, but access is local.

Regulation, Audits, and Tether’s Changing Structure

Tether’s history is a major reason USDT remains closely watched. In 2021, the U.S. Commodity Futures Trading Commission ordered Tether to pay $41 million over claims that USDT was fully backed by U.S. dollars. Tether misrepresented its reserves from at least June 1, 2016 to Feb. 25, 2019, and held sufficient fiat reserves for only 27.6% of days in a 26-month sample.

The New York Attorney General also reached a 2021 settlement with Bitfinex and Tether. The companies deceived clients and the market by overstating reserves and hiding about $850 million in losses around the world. The settlement required them to end trading activity with New Yorkers, pay $18.5 million in penalties, and provide additional reporting.

Tether International, S.A. de C.V. relocated from the British Virgin Islands to El Salvador in January 2025, became the sole issuer of fiat-denominated tokens, and obtained authorization as a stablecoin issuer and digital asset service provider under El Salvador’s Digital Asset Issuance Law.

Europe is a different story. The Markets in Crypto-Assets Regulation, known as MiCA, creates EU rules for crypto assets, including e-money tokens and asset-referenced tokens. National competent authorities were directed to ensure compliance by crypto-asset service providers regarding non-MiCA-compliant asset-referenced tokens and e-money tokens no later than the end of Q1 2025, with trading platforms expected to stop making non-compliant ARTs and EMTs available for trading and sell-only transitions allowed into the end of Q1 2025.

In the United States, the GENIUS Act became law in July 2025. The law created a federal stablecoin system, required 100% reserve backing with liquid assets such as U.S. dollars or short-term Treasuries, required monthly public reserve disclosures, and required issuers to comply with Bank Secrecy Act anti-money-laundering and sanctions obligations.

Tether responded to the U.S. framework with a separate U.S.-focused token. In January 2026, Tether launched USA₮, a federally regulated dollar-backed stablecoin designed to operate within the GENIUS Act framework and issued by Anchorage Digital Bank. That product is separate from global USDT, which remains the dominant Tether token in offshore and international crypto markets.

How To Buy, Hold, or Redeem USDT

Most people who want USDT will use an exchange, not Tether’s direct redemption system. A centralized exchange usually offers the simplest path because it can handle fiat deposits, trading pairs, network selection, and withdrawals in one interface. People comparing on-ramp safety can start with CryptoSlate’s safest crypto exchanges rankings.

A typical flow is straightforward. Choose an exchange that supports your region. Deposit fiat or another crypto asset. Buy USDT. Select the correct network before withdrawing. Send a small test amount if the destination is new. Keep records for tax and accounting.

Wallet choice depends on what you plan to do with the token. A custodial exchange account is easier for beginners, but the exchange controls withdrawals. A self-custody wallet gives you direct control of private keys, but mistakes are your responsibility. If you plan to use USDT on DeFi apps, CryptoSlate’s decentralized crypto exchanges guide can help explain where onchain swaps fit.

Direct redemption through Tether is a narrower route. Issuance and redemption require a verified Tether customer. The minimum acquisition or redemption amount is $100,000, with a redemption charge that starts at $1,000 and rises when 0.1% of the redemption is higher. That structure is built for institutions and high-volume users, not everyday cashouts.

Teams evaluating stablecoin rails for a product launch should treat USDT as part of a larger operating stack. Exchange access, liquidity, custody, compliance, network support, and user geography all matter.

FAQs

Can you stake USDT?

No. USDT cannot be staked natively because it is a reserve-backed stablecoin issued on multiple blockchain networks, not a proof-of-stake asset with validator rewards. Products marketed as “USDT staking” usually mean lending, exchange earn deposits, DeFi supply, or liquidity provision, each with separate terms and risk.

How can you earn USDT?

You can earn USDT through third-party products such as exchange earn accounts, lending products, DeFi money markets, liquidity pools, payment rewards, or verified campaigns. The yield normally comes from lending income, liquidity fees, exchange reward programs, or promotion budgets, not from USDT itself. Check product terms, regional eligibility, and redemption rules before depositing.

Is USDT staking the same as lending?

No. The phrase “USDT staking” is often a marketing label for lending or deposit products. Native staking secures a proof-of-stake network. USDT yield products usually involve lending USDT, supplying a protocol, or joining an exchange earn product. That means counterparty, custody, smart contract, rate, and redemption risks matter.

What are the risks of earning yield on USDT?

The risk set depends on the venue. Centralized products add platform and custody exposure. DeFi products add contract and liquidity exposure. All routes can face depeg pressure, changing rates, lockups, redemption windows, local restrictions, and network-selection mistakes when USDT moves between chains.

Can you get free USDT from faucets?

Faucets are not a dependable way to earn USDT. Some may pay tiny rewards, but many unverified sites use “free USDT” messaging to collect clicks, wallet permissions, deposits, or personal data. Treat faucet claims as security risks unless the operator, rules, and payout history are verified. This guide does not recommend faucet sites.

CryptoSlate does not provide investment, legal, tax, or accounting advice. Crypto assets can be volatile, stablecoins can lose access or liquidity, and users should verify official sources before transferring funds.